The US economic recovery, which began more than three years ago, has been at best erratic. Much of the media attention is currently focused on the impact of the fiscal cliff on the recovery, overshadowing other forces working in the economy. For its planning purposes the essential question your company needs to answer is “Is 2013 the year the recovery gains sustainable momentum?”

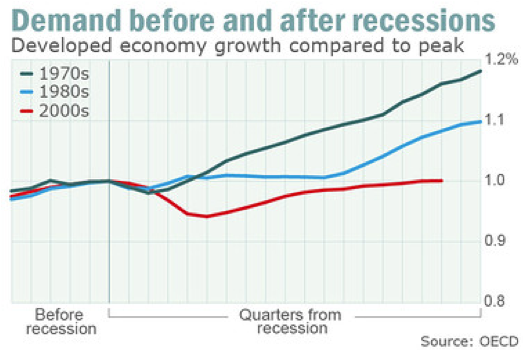

The US economy is recovering at a slow paste. Through this year, the US will likely see continued slow, steady gains in housing, employment, consumer spending, and consumer confidence. However, post-recession recovery has been taking a lot longer than it ever has. Out of the three major recessions that have hit the global economy since the 1970s, recovery from the current one that landed in the late 2000s has not been up to par, according to the Organization for Economic Cooperation and Development (OECD) latest Economic Outlook released on Tuesday, November 27.

This shows that in this last recession the US is lagging well behind prior recovery periods. However, it is difficult to put a finger on exactly what the problem is for the overall lag this time.

For starters, the financial crisis/recession terrified nearly all Americans from consumers to business owners. This caused them to react with caution and so consumers and business owners became risk-averse… spending less and saving more. This caused a disequilibrium in the product sector and the IS curve to shift to the left (Wealth¯, Planned Spending ¯® Output¯, unemployment, household income ¯). This then caused a disequilibrium in the financial sector and the LM curve to shift to the left (MD<MS, bonds, interest rates ¯®MD, consumption , investment® equilibrium), The increase in risk -aversion however caused the demand for money to increase which then led to the increase in interest rate and output to fall). This is when the US faced the Great Recession.

Usually, following a recession hits bottom, there's a period of above-average growth. However, this is not the case for the current US lagging economy. The U.S. economy has been slowly recovering from the severe financial crisis. U.S. real GDP growth has averaged about 2.2% in the current economic recovery, roughly half the normal pace of growth in post-recession recoveries. Other than people under forecasting the recessionary gap, the recession was accompanied by a financial crisis. However, the recovery lag we face now could be caused by three main fiscal issues in the U.S.: (1) the unsustainable multiyear pattern of persistent deficits and a rising debt-to-GDP ratio, (2) the uncertainty about the new tax rules which will prevail once a tax compromise is reached and (3) the euro-area crisis.

According to the Congressional Research Service (CRS) report (2012), though deficit levels are currently high, they are expected to fall towards the middle part of the decade as the economic recovery continues. Looking beyond this decade, however, the country’s fiscal outlook becomes more bleak as spending on programs like Social Security, Medicare, and Medicaid, and net interest are projected to consume a larger portion of the total federal budget. Uncertainty of what will happen with the federal budget causes a delay in the recovery. Delays in taking corrective action will exacerbate the size of the changes that need to be made.

Any choices that are made to address the budgetary imbalances have important economic, social, and generational impacts in the present and the future. In order to undertake any substantive changes to the federal policies and programs, sacrifices to favored programs and increases in taxes will likely be required. The sacrifices made today are essential to minimizing the size of potential programmatic cuts or tax increases, reducing the probability of a future crisis, and ensuring an improved standard of living for future generations.

This leads me to expect a similar slow post-recession recovery/outcome for 2013, with U.S. real GDP growth likely to be weaker in the first half and stronger in the second half. The reason I say growth will be weaker in the first half of 2013 is because there will likely be a recognition lag. A recognition lag is the time it takes to figure out where the economy is going in perspective to where we would like it to be. A clear indicator of the direction the economy is moving takes at least six months of data. Effects of both fiscal unsustainable patterns and uncertainties have consumers and business owners taking a wait-and-see approach before spending or investing. Once the government reaches an agreement on what they will do with the budget (change government spending, taxes and money supply) then they actually have implement them. This is called the legislative lag. After they implement each policy, the policy has to systematically work its way through the economy, which is called the effectiveness lag. This process takes a long time and is what brought me to my conclusion above.

Although I suspect from my research that there is a slow economic recovery, there is a visible recovery lag for 2013. The housing recovery has been very strong, maybe the strongest, with the low interest rates and plunging home prices (down about a third nationally). Construction spending rose 1.4 percent in October. Housing construction spending jumped 3 percent in October. Nonresidential building rose 0.3 percent. Sales of new homes fell slightly in October, dragged lower by steep declines in the Northeast partly related to Superstorm Sandy. New-home sales, however, were still 17 percent higher in October than the same month a year ago. From July through September, residential construction grew at an annual rate of 14.2 percent. Housing construction is on track to contribute to economic growth this year for the first time in the five years since the housing bubble burst. Though new homes represent only a fraction of the housing market, they have an out-size impact on the economy. Each home built creates an average of three jobs for a year and generates about $90,000 in tax revenue, according to statistics from the National Association of Home Builders (2012). Builders are increasingly confident that the housing recovery will endure. A measure of their confidence rose in November to the highest level in 6 1/2 years. And builders broke ground on new homes and apartments in October at the fastest pace in more than four years.

But there are factors dragging on the housing recovery. Many Americans, particularly first-time homebuyers, are unable to qualify for a mortgage. And many can't afford larger down payments that are being required by banks. While housing has strengthened this year, the broader economy has lagged behind. The government reported last week that overall economic growth increase to an annual rate of 2.7 percent in the July-September quarter, up from 1.3 percent in the April-June quarter.

So although the housing recovery caused spending, consumer confidence, builders confident, and unemployment to¯® Household income, Expectationand output… recovery is being restricted by factors that have lagged such as frustration over borrowing and lending. Consumers are frustrated by lenders who are maintaining "tight terms and conditions on mortgage loans, even for potential borrowers with relatively good credit"(Samuelson, 2012). This will cause the IS curve to shift up showing a higher output and GDP (although still below equilibrium)

Consumer confidence in the economy is at its strongest since early 2008 but although consumer confidence has improved it remains at low levels. The same applies to the economy. The U.S. economy has been stronger than anticipated, but it is still weak. According the Forbes article “U.S. Economy Stronger Than Thought, But Still Weak: Q3 GDP Growth Revised Higher To 2.7%”, the economy last quarter was stronger than originally forecast, driven by resilient consumers and a rare increase in government spending. Third quarter GDP expanded by an annualized 2.7%, which is greater than the first estimated of 2.0%. Vigorous shopping by consumers, especially during black Friday, had convinced economists that the earlier estimated was low. Economists had thought today’s revision would show 2.8% growth.

GDP offers the broadest snapshot possible of an economy because it’s the sum of all goods and services produced during the period. The 2.7% growth is a welcome number because it suggests consumers are holding up well under economic pressure. It remains weak, however, by traditional measures, and it will do little to meaningfully lower unemployment. Most economists say the country must grow more than 3% to make significant headway.

Consumer Spending increases but not so much. Household purchases climbed at a 1.4 percent rate, the smallest gain in more than a year. “The pace of consumer spending was disappointing, but it seems less worrisome given that some other sectors of the economy are doing better, like housing” said Chris Rupkey, chief financial economist at Bank of Tokyo- Mitsubishi UFJ Ltd (Chandra, 2012). Consumer confidence in the U.S. climbed to a seven-month high last week, and more Americans signed contracts in October to buy a previously owned house. An improving housing market may further lift spirits, benefiting stores such as Target Corp. and Macy’s Inc.

Again, consumer confidence increases, spending increases, unemployment decreases, household income increases, expectation increases and therefor output will increase, GDP will also increase (product sector shock)

As income increases, output increases, risk aversion decreases therefor money demand > money supply, interest rate decrease and again output increases (financial sector shock) and LM curve shifts down.

So far, fiscal uncertainties have had a different effect on companies than on consumers. Corporate decision-makers have shown a tendency to postpone the placement of capital spending orders. Such a negative response has not yet spread to consumers, although there is a risk that could occur this holiday season. So far, however, consumers have shown a willingness to purchase consumer goods and housing, despite slow income growth. One potential explanation is that layoffs have dropped, bolstering the job confidence of those still employed. During periods of labor market weakness, it has been weak hiring rather than intensified layoffs which have explained the weakness. The U.S. labor market has shown a sustained subdued expansion. Despite subcycles of shorter and faster growth, non-agricultural payroll employment has risen at a 157,000 per month pace so far this year, little changed from the 153,000 per month pace in 2011.

Another cause might be the euro-area crisis and what it called “slow and uneven” progress on needed policy action. Its budgetary crisis was "not anticipated." A decade ago, hardly anyone thought that advanced nations might default on their government debt. Now the possibility is openly discussed. Decisions about what to do about the financial crisis and recession in the “Eurozone” have been made relatively slowly, reflecting the differing interests among and within the 17 countries of the Eurozone. The Draghi plan at the European Central Bank has reduced the risk of a full-scale financial meltdown in Europe, but many underlying problems (relative competitiveness, balance of trade deficits and legacy debt burdens) have been managed rather than solved. Europe is expected to have a "less worse" economy in 2013, with a modest improvement from a full-scale recession in 2012 to flat economic activity in 2013.

As foreign income decreases, CAB decreases and therefor (EP) NX decreases < Ey therefor y decreases and Md decreases <Ms therefor decreases, EP increases therefor KAB decreases, D$decreases, e decreases therefor NX increases, CAB increases therefor EP increases

A recession with major initial US partners may cause an initial contraction through the US economy but as it does it will reverse itself (this might take a year or more). The US having a flexible exchange rate and an open market provides a safety net to the domestic economy. This will cause the Bp curve to shift up. The response of households and businesses to the crisis outside the US is very critical however. So far it seems that it has not had much effect on household confidence.

So to answer the question “Is 2013 the year the recovery gains sustainable momentum?” I would say 2013 is not the year the recovery gains sustainable momentum however I do think the economy will slowly recover. Although the economy is slowly recovering and GDP is slightly increasing there are still a lot of uncertainties in the economy that could be causing a time lag. Maybe once the US reduces its deficit and reduces uncertainty in the economy consumers can start to spend and businesses can start to invest. Patience will be the key to recovery!

Note: Economic lag can have a damaging effect on the economics of a country. Let’s assume the agreed upon budget did not help the recovery, a time lag will cause a delay between the identification of an economic problem and the establishment of a solution to the issue. However, if we assume that implemented budget was working then a fall in the unemployment rate would be considered a lagging indicator of economic recovery. That is, it occurred after other indicators of recovery, such as GDP growth. As such, job creation and lower unemployment show that the GDP growth has been, and will likely continue to be, sustained.

For starters, the financial crisis/recession terrified nearly all Americans from consumers to business owners. This caused them to react with caution and so consumers and business owners became risk-averse… spending less and saving more. This caused a disequilibrium in the product sector and the IS curve to shift to the left (Wealth¯, Planned Spending ¯® Output¯, unemployment, household income ¯). This then caused a disequilibrium in the financial sector and the LM curve to shift to the left (MD<MS, bonds, interest rates ¯®MD, consumption , investment® equilibrium), The increase in risk -aversion however caused the demand for money to increase which then led to the increase in interest rate and output to fall). This is when the US faced the Great Recession.

Usually, following a recession hits bottom, there's a period of above-average growth. However, this is not the case for the current US lagging economy. The U.S. economy has been slowly recovering from the severe financial crisis. U.S. real GDP growth has averaged about 2.2% in the current economic recovery, roughly half the normal pace of growth in post-recession recoveries. Other than people under forecasting the recessionary gap, the recession was accompanied by a financial crisis. However, the recovery lag we face now could be caused by three main fiscal issues in the U.S.: (1) the unsustainable multiyear pattern of persistent deficits and a rising debt-to-GDP ratio, (2) the uncertainty about the new tax rules which will prevail once a tax compromise is reached and (3) the euro-area crisis.

According to the Congressional Research Service (CRS) report (2012), though deficit levels are currently high, they are expected to fall towards the middle part of the decade as the economic recovery continues. Looking beyond this decade, however, the country’s fiscal outlook becomes more bleak as spending on programs like Social Security, Medicare, and Medicaid, and net interest are projected to consume a larger portion of the total federal budget. Uncertainty of what will happen with the federal budget causes a delay in the recovery. Delays in taking corrective action will exacerbate the size of the changes that need to be made.

Any choices that are made to address the budgetary imbalances have important economic, social, and generational impacts in the present and the future. In order to undertake any substantive changes to the federal policies and programs, sacrifices to favored programs and increases in taxes will likely be required. The sacrifices made today are essential to minimizing the size of potential programmatic cuts or tax increases, reducing the probability of a future crisis, and ensuring an improved standard of living for future generations.

This leads me to expect a similar slow post-recession recovery/outcome for 2013, with U.S. real GDP growth likely to be weaker in the first half and stronger in the second half. The reason I say growth will be weaker in the first half of 2013 is because there will likely be a recognition lag. A recognition lag is the time it takes to figure out where the economy is going in perspective to where we would like it to be. A clear indicator of the direction the economy is moving takes at least six months of data. Effects of both fiscal unsustainable patterns and uncertainties have consumers and business owners taking a wait-and-see approach before spending or investing. Once the government reaches an agreement on what they will do with the budget (change government spending, taxes and money supply) then they actually have implement them. This is called the legislative lag. After they implement each policy, the policy has to systematically work its way through the economy, which is called the effectiveness lag. This process takes a long time and is what brought me to my conclusion above.

Although I suspect from my research that there is a slow economic recovery, there is a visible recovery lag for 2013. The housing recovery has been very strong, maybe the strongest, with the low interest rates and plunging home prices (down about a third nationally). Construction spending rose 1.4 percent in October. Housing construction spending jumped 3 percent in October. Nonresidential building rose 0.3 percent. Sales of new homes fell slightly in October, dragged lower by steep declines in the Northeast partly related to Superstorm Sandy. New-home sales, however, were still 17 percent higher in October than the same month a year ago. From July through September, residential construction grew at an annual rate of 14.2 percent. Housing construction is on track to contribute to economic growth this year for the first time in the five years since the housing bubble burst. Though new homes represent only a fraction of the housing market, they have an out-size impact on the economy. Each home built creates an average of three jobs for a year and generates about $90,000 in tax revenue, according to statistics from the National Association of Home Builders (2012). Builders are increasingly confident that the housing recovery will endure. A measure of their confidence rose in November to the highest level in 6 1/2 years. And builders broke ground on new homes and apartments in October at the fastest pace in more than four years.

But there are factors dragging on the housing recovery. Many Americans, particularly first-time homebuyers, are unable to qualify for a mortgage. And many can't afford larger down payments that are being required by banks. While housing has strengthened this year, the broader economy has lagged behind. The government reported last week that overall economic growth increase to an annual rate of 2.7 percent in the July-September quarter, up from 1.3 percent in the April-June quarter.

So although the housing recovery caused spending, consumer confidence, builders confident, and unemployment to¯® Household income, Expectationand output… recovery is being restricted by factors that have lagged such as frustration over borrowing and lending. Consumers are frustrated by lenders who are maintaining "tight terms and conditions on mortgage loans, even for potential borrowers with relatively good credit"(Samuelson, 2012). This will cause the IS curve to shift up showing a higher output and GDP (although still below equilibrium)

Consumer confidence in the economy is at its strongest since early 2008 but although consumer confidence has improved it remains at low levels. The same applies to the economy. The U.S. economy has been stronger than anticipated, but it is still weak. According the Forbes article “U.S. Economy Stronger Than Thought, But Still Weak: Q3 GDP Growth Revised Higher To 2.7%”, the economy last quarter was stronger than originally forecast, driven by resilient consumers and a rare increase in government spending. Third quarter GDP expanded by an annualized 2.7%, which is greater than the first estimated of 2.0%. Vigorous shopping by consumers, especially during black Friday, had convinced economists that the earlier estimated was low. Economists had thought today’s revision would show 2.8% growth.

GDP offers the broadest snapshot possible of an economy because it’s the sum of all goods and services produced during the period. The 2.7% growth is a welcome number because it suggests consumers are holding up well under economic pressure. It remains weak, however, by traditional measures, and it will do little to meaningfully lower unemployment. Most economists say the country must grow more than 3% to make significant headway.

Consumer Spending increases but not so much. Household purchases climbed at a 1.4 percent rate, the smallest gain in more than a year. “The pace of consumer spending was disappointing, but it seems less worrisome given that some other sectors of the economy are doing better, like housing” said Chris Rupkey, chief financial economist at Bank of Tokyo- Mitsubishi UFJ Ltd (Chandra, 2012). Consumer confidence in the U.S. climbed to a seven-month high last week, and more Americans signed contracts in October to buy a previously owned house. An improving housing market may further lift spirits, benefiting stores such as Target Corp. and Macy’s Inc.

Again, consumer confidence increases, spending increases, unemployment decreases, household income increases, expectation increases and therefor output will increase, GDP will also increase (product sector shock)

As income increases, output increases, risk aversion decreases therefor money demand > money supply, interest rate decrease and again output increases (financial sector shock) and LM curve shifts down.

So far, fiscal uncertainties have had a different effect on companies than on consumers. Corporate decision-makers have shown a tendency to postpone the placement of capital spending orders. Such a negative response has not yet spread to consumers, although there is a risk that could occur this holiday season. So far, however, consumers have shown a willingness to purchase consumer goods and housing, despite slow income growth. One potential explanation is that layoffs have dropped, bolstering the job confidence of those still employed. During periods of labor market weakness, it has been weak hiring rather than intensified layoffs which have explained the weakness. The U.S. labor market has shown a sustained subdued expansion. Despite subcycles of shorter and faster growth, non-agricultural payroll employment has risen at a 157,000 per month pace so far this year, little changed from the 153,000 per month pace in 2011.

Another cause might be the euro-area crisis and what it called “slow and uneven” progress on needed policy action. Its budgetary crisis was "not anticipated." A decade ago, hardly anyone thought that advanced nations might default on their government debt. Now the possibility is openly discussed. Decisions about what to do about the financial crisis and recession in the “Eurozone” have been made relatively slowly, reflecting the differing interests among and within the 17 countries of the Eurozone. The Draghi plan at the European Central Bank has reduced the risk of a full-scale financial meltdown in Europe, but many underlying problems (relative competitiveness, balance of trade deficits and legacy debt burdens) have been managed rather than solved. Europe is expected to have a "less worse" economy in 2013, with a modest improvement from a full-scale recession in 2012 to flat economic activity in 2013.

As foreign income decreases, CAB decreases and therefor (EP) NX decreases < Ey therefor y decreases and Md decreases <Ms therefor decreases, EP increases therefor KAB decreases, D$decreases, e decreases therefor NX increases, CAB increases therefor EP increases

A recession with major initial US partners may cause an initial contraction through the US economy but as it does it will reverse itself (this might take a year or more). The US having a flexible exchange rate and an open market provides a safety net to the domestic economy. This will cause the Bp curve to shift up. The response of households and businesses to the crisis outside the US is very critical however. So far it seems that it has not had much effect on household confidence.

So to answer the question “Is 2013 the year the recovery gains sustainable momentum?” I would say 2013 is not the year the recovery gains sustainable momentum however I do think the economy will slowly recover. Although the economy is slowly recovering and GDP is slightly increasing there are still a lot of uncertainties in the economy that could be causing a time lag. Maybe once the US reduces its deficit and reduces uncertainty in the economy consumers can start to spend and businesses can start to invest. Patience will be the key to recovery!

Note: Economic lag can have a damaging effect on the economics of a country. Let’s assume the agreed upon budget did not help the recovery, a time lag will cause a delay between the identification of an economic problem and the establishment of a solution to the issue. However, if we assume that implemented budget was working then a fall in the unemployment rate would be considered a lagging indicator of economic recovery. That is, it occurred after other indicators of recovery, such as GDP growth. As such, job creation and lower unemployment show that the GDP growth has been, and will likely continue to be, sustained.

References

Chandra, S. (2012, November 29). Consumer Spending in U.S. Grows Less Than Forecast - Bloomberg. Bloomberg - Business, Financial & Economic News, Stock Quotes. Retrieved December 4, 2012, from http://www.bloomberg.com/news/2012-11-29/economy-in-u-s-grew-at-2-7-rate-more-than-first-estimated.html

Compared to prior recessions, this time the bounce back is taking longer: OECD - The Tell – Market Watch. (2012, November 27). Stock Market Commentary - Economic Articles - Business Articles. Retrieved December 3, 2012, from http://blogs.marketwatch.com/thetell/2012/11/27/post-recession-recovery-is-taking-a-lot-longer-this-time-says-oecd/

U.S. Economy Stronger Than Thought, But Still Weak: Q3 GDP Growth Revised Higher To 2.7% - Forbes. (2012, November 29). Information for the World's Business Leaders - Forbes.com. Retrieved December 3, 2012, from http://www.forbes.com/sites/abrambrown/2012/11/29/us-economy-stronger-than-thought-but-still-weak/

U.S. builders in October lifted spending 1.4 percent - CBS News. (2012, December 3). Breaking News Headlines: Business, Entertainment & World News - CBS News. Retrieved December 3, 2012, from http://www.cbsnews.com/8301-505123_162-57556865/u.s-builders-in-october-lifted-spending-1.4-percent/

Chandra, S. (2012, November 29). Consumer Spending in U.S. Grows Less Than Forecast - Bloomberg. Bloomberg - Business, Financial & Economic News, Stock Quotes. Retrieved December 4, 2012, from http://www.bloomberg.com/news/2012-11-29/economy-in-u-s-grew-at-2-7-rate-more-than-first-estimated.html

Compared to prior recessions, this time the bounce back is taking longer: OECD - The Tell – Market Watch. (2012, November 27). Stock Market Commentary - Economic Articles - Business Articles. Retrieved December 3, 2012, from http://blogs.marketwatch.com/thetell/2012/11/27/post-recession-recovery-is-taking-a-lot-longer-this-time-says-oecd/

U.S. Economy Stronger Than Thought, But Still Weak: Q3 GDP Growth Revised Higher To 2.7% - Forbes. (2012, November 29). Information for the World's Business Leaders - Forbes.com. Retrieved December 3, 2012, from http://www.forbes.com/sites/abrambrown/2012/11/29/us-economy-stronger-than-thought-but-still-weak/

U.S. builders in October lifted spending 1.4 percent - CBS News. (2012, December 3). Breaking News Headlines: Business, Entertainment & World News - CBS News. Retrieved December 3, 2012, from http://www.cbsnews.com/8301-505123_162-57556865/u.s-builders-in-october-lifted-spending-1.4-percent/

RSS Feed

RSS Feed